Introduction

In the first three units, you have learnt how to identify

sources of school funds, budget for and secure the funds. Financial

management, amongst other things, involves recognising and respecting

authorities, regulations and practices governing the receiving,

keeping and spending of funds. In this unit you will learn about

the basic framework and mechanisms of financial management and

gain experience in applying appropriate financial management

practices and skills.

Individual study time: 6 hours

Learning outcomes

By the end of this unit you should be able to:

• describe the basic framework of financial management

• state the authorities, rules and regulations governing

school funds and the receiving and banking of school funds

• describe the practices for book-keeping in schools

and the use of inventories

• outline safeguards for the security of school funds.

Basic framework of financial management

Activity 4.1

Before you proceed to look at Unit 4 in detail, please revise

Units 2 and 3 by looking back on the sources of funds for your

school budget and answering the following questions:

(1) How much funding did you secure from each source?

(2) Which source was most reliable? Why?

(3) Over what period did the funds come into the school?

(4) Is the amount collected more or less than budgeted?

If less, how and when do you envisage filling the gap or achieving

your planned target?

(5) Are your priorities still the same?

Comments

You will realise that funds coming into a school are not entirely

certain and are often not adequate. To manage these limited

funds, the school head, as a public employee and the accounting

officer, must be guided by the basic framework and mechanisms

of financial managment.

Framework for managing school funds

Activity 4.2

(1) Considering your school, identify and describe the framework

in which you as a head manage the school funds.

(2) How flexible are you in deciding what to spend funds on

and under what circumstance?

(3) How free are you to make purchases?

(4) What are the national as well as school financial policies

within which you operate?

(5) How do you allocate funds and operate votes?

Comments

Your answers in the above activities are likely to bring out

and include the following:

Keeping accurate financial information

You are expected to keep complete and accurate financial information

and to present this information properly. This information

should include sources of revenue and accurate entry of expenditure,

avoiding errors or omissions as much as possible. Proper presentation

further demands that you always put any required financial

information under the correct heading and in the correct place.

The information should be arranged under broad headings,

such as transport, and then put under smaller headings, such

as petrol and vehicle maintenance. Preferably you should present

the information under appropriate, clearly understood headings

in a layout based on the way in which education is actually

provided. This will enable you to compare costs of the range

of services offered by the school.

Flexibility and freedom with responsibility

In managing school funds, you should enjoy some financial

freedom and flexibility to enable you consider a range of

options. This demands a high sense of responsibility in order

to use the freedom and flexibility effectively.

Virement (switching expenditure)

In a school with a well-organised financial management system

overall types of virement can be applied. Under this system

you, as the head of the school, can always agree with the

governing bodies to switch expenditure between one heading

and another if they so wish and if need be.

This depends on how you have prioritised the school services.

Purchasing Freedom

It is important for you as the head to enjoy freedom of purchase.

Lack of purchasing freedom restricts the freedom of schools

as consumers and delays the purchasing process.

Financial Policies

The school should have financial policies to guide the financial

administrators and managers. These policies will assist financial

control and regulate the processes of receipting, keeping,

withdrawing and expending funds. However these policies should

not clash with the official national policies on school finances.

Proper allocation of funds

To manage the school finances you should be conversant with

what each department has and what it needs. Involving teachers

and heads of department in this process is very important.

Authorities, rules and regulations governing school funds

It is important that you are equally conversant with the

authorities, rules and regulations that should guide you in

the effective handling of school funds.

Tuition fees

Activity 4.3

Reflecting upon the situation in your school:

(1) Who establishes the level of school fees? Where is this

stipulated?

(2) Who pays tuition fees to the school?

(3) What rules and regulations governing fees, originate at:

- national;

- district;

- school level?

(4) To whom is the school head accountable over tuition fees?

Comments

Tuition fees are gazetted, therefore government is the authority

for these funds, which must be expended as the law dictates.

In the above activity your response might have indicated that

at national level, relevant government authorities are likely

to determine the level of fees, sources of fees and their

purpose.

At district level, the District Education Officer and Treasurer

are likely to monitor the use of fees in schools under their

jurisdiction. In some cases they may determine the level and

purpose of the fees. Whereas at school level, the management

committee or board of governors decides on specific items

to be purchased and guides you the head to purchase and account

for the fees. This information should be found in government

statutes and standing instructions.

Grants

Activity 4.4

Grants are funds that government or other non-government organisations

give to run schools. Reflecting on your school situation:

(1) List the various sources of grants to your school.

(2) What activities or items are financed from grants in your

school?

(3) Who decides on how to spend the grants?

Comments

Guidelines on the management of grants are usually contained

in the rules and regulations of school governing bodies. Grants

are managed and controlled in a similar way to school fees

except that they have to be spent for the purpose(s) indicated

against the grant. Some grants have specific uses, for example,

salaries; other grants may be spent flexibly for example,

block grant.

PTA or community group funds

Activity 4.5

(1) Does your school receive Parent-Teacher Association funds?

(2) If so, how are PTA. charges levied and controlled?

(3) What items are financed from PTA funds in your school?

(4) What other community groups contribute funds to your school?

Comments

Your answers might have included the following:

1 PTA funds are not government gazetted fees.

2 They include funds that are voluntarily paid by parents

as decided in the general meeting of the PTA.

3 The funds are levied for the purpose agreed upon by the

members of the association but approved by the school management

committee or governing board.

Since you are the day-to-day administrator of the school,

the responsibility for collecting and banking this money rests

upon you, and you are accountable to the executive of the

committee and the electorate. The management committee or

the board of governors controls the PTA funds by ensuring

that the money is expended in the manner and for the purpose

agreed upon by the members of the PTA and approved by the

governing body of the school.

Other funds

Activity 4.6

(1) List other sources of funds for your school.

(2) Do you declare funds from extra sources to school authorities?

(3) Who decides on their use?

(4) Do you include them in your budget?

Comments

All funds obtained from other sources are also controlled

by the school governing body, that is the school management

committee or board of governors, which must sanction their

expenditure. You are the accounting officer of the school

for these funds.

Receiving and banking of school funds

It is clear that funds coming into the school must be

received according to set procedures and kept safely. A receipt

book is one of the commonest books of account. It is used

in the process of receiving funds into a school.

Receiving funds

Activity 4.7

(1) Describe how you officially receive money in your school.

(2) What kind of information do you record about funds received?

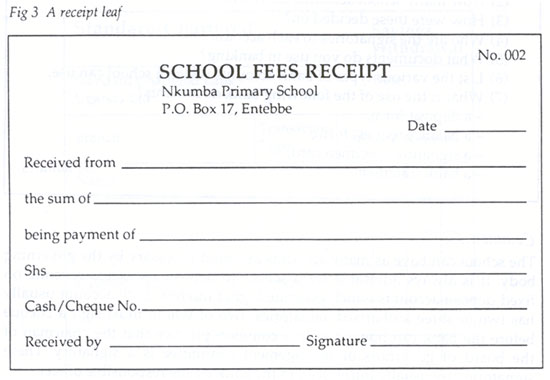

(3) Look at the receipt leaf shown in Fig 3 and list the main

information included on it.

(4) Describe the use of a receipt.

Fig 3 A receipt leaf

Comments

Typically in a school, funds come in cash, cheque or drafts.

These monies must be received properly and kept safely.

A receipt book is designed for receiving real cash or cheques.

A receipt must be made or written out immediately on receiving

the cash money or cheque, and the original should be sent

or given to the person(s) who has/have made the payment.

A receipt is used in a school to:

• acknowledge receipt of cash or cheque in settlement

of school dues

• to provide proof to the school that the student has

paid

• provide information for the cash book.

It bears the following basic information:

• the name of the person who paid the funds

• the name of the person who received the funds

• date received

• purpose of the funds

• type of funds (cash, cheque, etc.).

If money has to be kept before banking, it must be under

lock and key or in a safe to avoid theft or damage by fire,

etc.

Banking

The head of the school should first bank all school funds

and then withdraw as and when necessary. You should avoid using

cash before it is banked as much as possible.

Activity

4.8

For your school:

(1) How do you open an account?

(2) How many school accounts do you have?

(3) How were these decided on?

(4) Who are the signatories to each account?

(5) What documents do you use in banking?

(6) List the various types of bank accounts which a school can

use.

(7) What is the use of the following bank documents?

- a deposit form;

- a balance request form;

- a signature specimen card;

- a bank statement.

Comments

The school can have as many accounts as found necessary by

the governing body. It is always advisable for a school to

deposit its excess revenue on fixed deposit accounts which

generate higher interest. Each account usually has two or

three authorised signatories, two of whom must sign a cheque

before the bank can honour it. It is common practice that

the chairman of the board of governors or management committee

is a signatory. These signatories are usually introduced to

the bank by the responsible officer.

The following are some of the bank accounts that can be opened

and used by schools:

1 Current accounts (of various types) have deposit books both

for cash and for cheques. Cheque books are used for withdrawals

or transfer of deposits. Interest payment on the balance is

usually high, for example, 20 per cent per annum.

2 Savings accounts.

3 Fixed deposit accounts/time receipts, where the customer

is given a receipt and is only allowed to withdraw the money

when the receipt matures.

Withdrawing funds

Activity 4.9

(1) What bank and school regulations govern withdrawal of funds

in:

- current accounts;

- savings accounts;

- fixed deposit accounts?

(2) Describe the steps you usually take to draw money for your

school.

(3) On a cheque, identify the branch, the account number, the

cheque number and the drawer and payee.

Comments

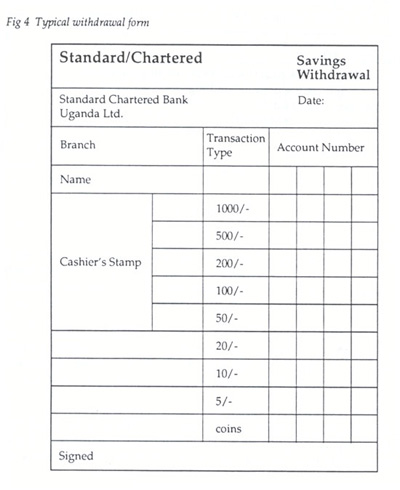

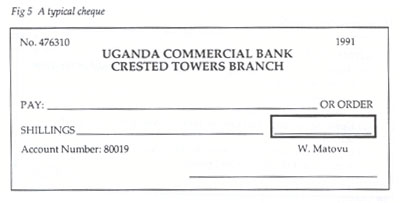

Funds are withdrawn using a withdrawal form or a cheque leaf.

A typical withdrawal form is shown in Fig 4 and a typical cheque

leaf in Fig 5.

A cheque is a written order directing the bank or bankers

to pay money as therein stated.

Fig 5 A typical cheque

Book-keeping

To facilitate accountability and keep records and to enhance

planning and overall financial performance, the school must

keep clear and accurate information of all its financial transactions.

This is called book-keeping.

Activity 4.10

(1) List all books of accounts which you use in your school.

(2) Which of these are used in handling

- the receiving of funds;

- the withdrawing of funds;

- expenditure;

- balances?

Comments

Your list of books may have included the following:

Vote books

This is a book in which records of items and amounts of money

approved to be expended per term are kept. This book should

be consulted before spending is undertaken, as is it a safeguard

against overspending in any one area.

Vouchers

Before payments are made, vouchers have to be written. A voucher

explains the reasons and authority for the expenditure. A

school should have and keep vouchers showing the details of

financial transactions in the school.

Local Purchase Order (LPO)

The LPO is used for identifying and authorising local purchases

voted for in the school. This is an agreement made between

the school and a supplier that the school is ready to purchase

the item at an agreed price. The LPO book should always be

kept under lock and key as some bad elements may use it wrongly.

Cash Book

This is the book where all cash transactions are recorded

each day.

Green Book/Petty cash

Money which is disbursed for official purposes is recorded

in the green book or petty cash book.

Cheque book

A cheque is a written order directing the bank or bankers

to pay money as therein stated. One should insist on obtaining

receipts for any payments made by the school. Where official

receipts are not available it is advisable to use petty cash

vouchers to serve as written statements supporting the expenditure.

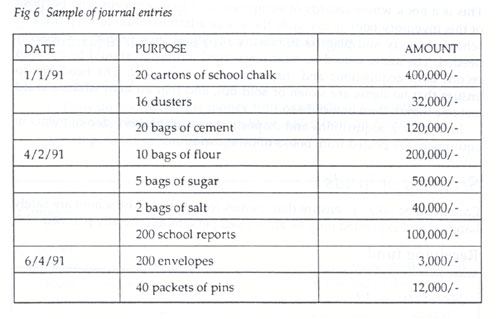

Journal

It is very important for a school head to record all financial

transactions in the journal. The journal has to be written

every day. This is the first step of the accounting cycle

of the school. See Figure 6.

Financial Ledgers

These are the books where the head of the school posts the

information provided in the journals. The purpose of ledgers

is for recording the financial transactions of a school as

they occur. See details on page 45.

Trial Balance

This is the list of all the accounts used by the school. It

is used to summarise the effect of all transactions on the

school accounts and show how each account is being used.

Trial balances help heads know the balances of each account

and whether the school's records match those of the bank.

Also they help check whether budgets are being adhered to.

Financial Statements

These are the statements made by the head to convey information

on the financial position of the school at a particular time.

Often they are presented to the board of governors for discussion.

Balance Sheet

This is the financial statement produced at the end of the

school year which shows the financial position of the school.

The normal practice is that the head of the school submits

the balance sheets to the authority that approved the school

budget, that is, the board of governors.

Income Statement

The income statement summarises the extenet to which profits

or losses in an account are occurring. In it, revenues and

expenditures are compared in order to project the profits

or losses. It is also prepared at the end of the financial

year.

Black Book

This is a record of the outstanding debts of the school.

General Stores Inventory Book

This is a book where records of equipment and tools are kept.

The purpose of this inventory book is to enable the school

administration to keep track of school property and plan for

the future supply of such property whenever needed. The items

should be clearly arranged. Provision should be made to record

both acquisitions and dispositions of items kept. The head

has to ensure that no items are stolen or sold out, and that

an item which should last one month does in fact do so.

In this book acquisitions and dispositions resulting from

deployments in equipment are posted from books of inventories.

Security of funds

Care must be taken to ensure that monies received into

the school are safely handled and expended only by authorised

persons as officially planned.

Receiving funds

Activity 4.11

(1) Where do you keep your cash, etc. in the school?

(2) What safety precautions does your school have?

(3) What financial risks are likely to occur in your school?

Comments

Cash or sensitive books of accounts must be kept under lock

and key and if possible, in a strong safe to guard against

fire, theft, burglary, forgery and pests.

During banking

Ensure that you carefully fill in banking forms and retain

and file copies of the deposit forms. Also note:

Bank Statements/Bank Reconciliation

These must be received on a monthly basis and compared with

what is in the ledger and these must agree. Any discrepancies

must be reported to the bank manager immediately.

Account Balance

The bursar should always ask for the account balance when

he comes to the bank. This account must be signed by the manager

and the accountant, and not the ledger keepers. Why?

Bank staff

The bursar should avoid getting used to one bank staff member

doing everything as this encourages forgery, or complicity.

Stop payments

Once the cheque book is misplaced or has some leaves missing,

immediate report should be made to the bank to stop payment,

otherwise the money can be paid to wrong elements.

Withdrawal of funds and prevention of forgery

Activity 4.12

(1) How do you withdraw money from your school accounts?

(2) List ways in which money could be stolen from an account.

(3) List possible precautions against these.

Comments

Cheques

1 When you write the figures in words on a cheque, there should

be no space in between the words. Any space left at the end

of the word 'only' should be covered with one ruled line.

2 The amount in figures and all parts of the cheque must

be clearly written and the remaining areas uncovered should

be covered by double ruled lines.

3 The following figures should be watched carefully as they

can easily be forged: 9, nine(ty) 8, eight(y) 7, seven(ty)

6, six(ty) 4, four(ty).

4 Change of signatories should be communicated to the bank

immediately.

5 Any alteration on the cheque must be countersigned by both

signatories. However, where the alteration involves altering

both the amount in words and in figures, a fresh cheque should

be written and the wrong one cancelled.

6 The counterfoil must be countersigned by both signatories

and the amount on the cheque must agree with the amount on

the counterfoil. It is important to write at the back of the

counterfoil the reason for the withdrawal.

7 The cheque book and all important accounting documents

and banking documents must be kept under lock and key by the

responsible officer.

8 No cheque leaf must be signed when blank as this can be

stolen and used in forgery.

9 Every time a cheque is written the remaining cheque leaves

must be counted and must also be used in their serial order.

Watch out for cheques taken from the back of the book!

10 For cash cheques both the face and the back must be signed

by both signatories and must bear the title of account on

both sides. The person receiving the cash must have his/her

name and identity written by him or her and signed at the

back of the cheque.

11 A school cheques should normally require at least two

signatories - either the head of school or deputy and the

person concerned with school book-keeping, in other words

the bursar.

Using carbon paper

All financial papers should be signed directly and not on

a carbon, as an unscrupulous clerk can put some blank vouchers

in and the officer will sign.

Signing without security

No voucher or cheque should be signed without first scrutinising

it. Signing when one is too busy or too tired can encourage

lack of security.

Signatures

Signatures should not be so simple that they can easily be

forged. Many people keep two signatures - one for bank purposes

and one for other duties.

Saving Accounts

The person depositing should ensure that the bank employee

initials or signs for the balance posted in the passbook,

as sometimes the passbook may be posted when actually the

deposit slip has been destroyed and money taken. Periodically

the balance in the passbook should be compared with that on

the bank's ledger card.

Summary

In this unit you have learnt the following:

1 School funds are managed within specific authority guidelines

and a framework which must be clearly known.

2 School heads must learn to receive and bank school funds

properly.

3 Books of accounts of school fees must be kept properly.

4 All possible care should be taken to ensure security of

funds.

|